Credit cards aren’t just a way to pay for things — they’re a subtle psychological game.

A lot of people believe they’re in control when they swipe, tap, or click “buy now,” but the truth is that these little pieces of plastic are designed to bypass some of the most important decision-making systems in your brain. And the companies behind them? They know exactly what they’re doing.

If you’ve ever ended a month wondering, How did my bill get this high?, you’ve felt the quiet, invisible pull of how your brain interacts with credit. It’s not about being careless or “bad with money.” It’s about understanding that the way we process spending is deeply human — and deeply influenced by how the payment is made.

In this article, we’re going to explore that world in detail. I’m going to take you inside the mechanics of the mind, show you how emotions, marketing, and even neuroscience are all wrapped up in your credit card habits, and most importantly, I’m going to give you real strategies to flip the script so you can make your card work for you, not against you.

Why a Card Never Feels Like “Real Money”

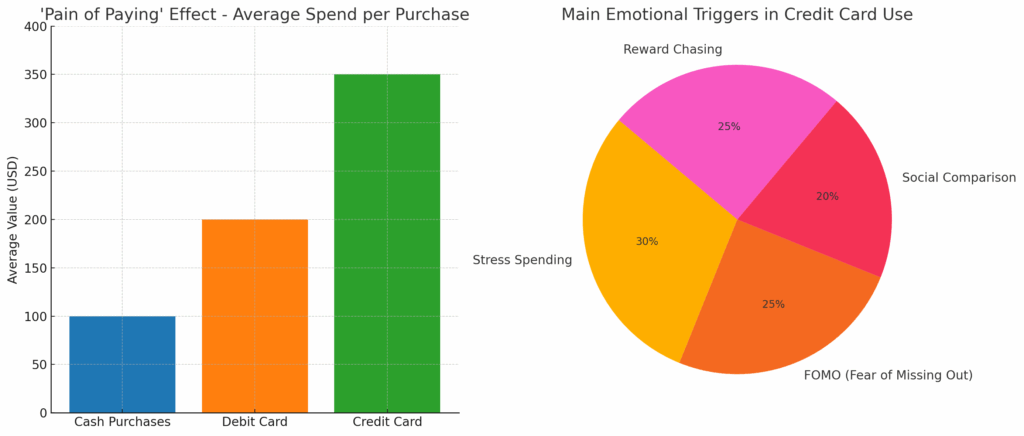

Have you ever noticed that paying cash feels heavier? When you hand over a $100 bill, there’s a tiny twinge in your gut. That’s not your imagination — it’s your brain reacting to loss.

Psychologists call this the pain of paying. It’s a very real sensation processed in the insular cortex, the part of your brain linked to negative feelings and pain perception. When you use cash, the pain is immediate and tangible. You see the money leaving your hands, and your brain instantly logs it as “less wealth.”

Credit cards remove that pain. There’s no physical exchange, just a swipe or tap. The loss isn’t immediate — it’s delayed until the bill arrives weeks later. That delay creates decoupling: your brain separates the joy of buying from the pain of paying. And when those two are disconnected, you spend more.

The Little Tricks That Make You Spend More

It’s not just about how the card works — it’s also about how retailers and banks structure the buying experience to keep you spending.

- Contactless payments: No signature, no PIN — just tap and go. Faster transactions mean less time to reconsider.

- One-click purchases online: Amazon mastered this. Once your card is saved, it’s easier to buy than to think twice.

- Minimum payment options: They frame your debt in tiny, harmless-looking numbers, making big purchases seem affordable.

- Rewards programs: Every swipe comes with a “prize” — points, miles, cashback — triggering the same reward pathways as gambling wins.

Every one of these reduces friction. And in psychology, the less friction there is before a behavior, the more likely you are to do it.

The Emotional Side of Credit Card Spending

We like to believe our purchases are rational. The truth? Most are emotional, and the card just makes it easier to act before we think.

- Stress Spending: That moment when a bad day makes you think, “I deserve this.”

- FOMO: The flash sale ending in 3 hours, the “only 2 left” warning on a product page. Scarcity pushes you to act now.

- Social Comparison: Seeing others with the latest phone, clothes, or trip photos makes you feel like you’re falling behind.

- Reward Chasing: “If I spend just $200 more, I’ll reach the next points tier.” You spend extra to “earn” — often more than the rewards are worth.

The emotional side is powerful because it bypasses logic. And credit cards are the perfect partner for that: they remove the immediate consequence, letting the emotional decision happen unchallenged.

Mental Accounting: The Illusion That Justifies Overspending

One of the most fascinating concepts in behavioral economics is mental accounting — the way we categorize money in our minds.

It’s why you might blow a $500 bonus on a weekend trip but hesitate to spend $500 from your paycheck on the same thing. It’s “extra money” in your mental books, even though it’s all the same in reality.

Credit cards feed into this illusion. You might use one card for “fun” and another for “essentials,” telling yourself you’re managing your budget well. But at the end of the month, both balances hit your actual finances.

Anchoring and the First Price You See

If the first TV you look at costs $3,000, the $1,800 one next to it feels cheap, even if it’s still expensive. That’s anchoring bias — your brain using the first number it sees as a baseline for comparison.

When you’re paying with cash, you might stop and think, “That’s still a lot of money.” But with a card? The lack of immediate pain makes the anchor even more powerful, pushing you toward higher prices.

Practical Ways to Outsmart the System

If you know the psychological plays, you can start defending yourself. Here’s what actually works in daily life:

- 24-Hour Rule: For non-essential buys, wait a full day. Most emotional purchases fade in importance.

- Delete Saved Cards Online: Force yourself to enter details manually. That pause is enough to reconsider.

- Lower Limits on Purpose: Less available credit means less room to dig a hole.

- Track in Real Time: Use apps or a spreadsheet so you see the running total before the bill arrives.

- Accountability Partner: Share your spending goals with someone you trust and check in weekly.

The Dopamine Factor

Every purchase triggers dopamine — the brain’s reward chemical. It’s why buying feels good, and anticipating a purchase can feel just as exciting. Credit cards amplify this because they strip away the immediate “loss” feeling.

Instead of letting dopamine lead you into overspending, you can redirect it. Gamify saving. Track streaks of no-spend days. Reward yourself with something meaningful only after hitting a financial goal — and pay for that reward with cash so you feel it.

Another reason credit cards feel so deceptively “easy” is because they blur the connection between value and price. When you pay cash, you can see the physical size of your payment. You can compare a thick stack of bills to what you’re buying and instinctively feel if it’s “worth it.”

With cards, that connection is gone. You’re not thinking about how many hours you worked to earn that $150 pair of shoes — you’re thinking about how good they’ll look or how comfortable they’ll feel. The exchange feels cleaner, but it’s also emptier, and that emptiness makes it easy to fill with more purchases.

How Stores and Brands Hack Your Brain

Retailers have been studying human psychology for decades. They know exactly how to encourage you to swipe your card more often. Here are just a few of the methods they use:

- Upselling at the Checkout: “Would you like to add a warranty for just $29?” In the moment, it feels tiny compared to your total purchase — your brain says yes before realizing those small yeses add up.

- Bundling: Combining items into a “deal” so you feel you’re saving money, even if you weren’t going to buy all the items individually.

- Pre-Sale Access for Cardholders: Special treatment for using your card makes you feel valued, encouraging loyalty — and more swipes.

- Point Expiry Dates: Creating urgency by making you use points or miles before they expire, even if it means spending unnecessarily.

They’re not just selling products — they’re selling moments where your brain chooses instant gratification over long-term sense.

The Lifestyle Inflation Trap

When people start earning more, their spending usually rises to match — a concept known as lifestyle inflation. Credit cards make this shift even smoother because they expand your perceived capacity to buy now and figure it out later.

The danger is that lifestyle inflation doesn’t always make you happier. Studies show that after a certain point, more spending adds little to your overall life satisfaction. But the momentum of “I can afford it now” is strong, and credit cards make it feel even more normal.

Breaking the Emotional Buying Cycle

If you want to truly master credit card psychology, you have to go deeper than budgeting apps or spending limits — you need to interrupt the emotional process that leads to swiping in the first place.

- Recognize Your Triggers — Keep a journal for a month and note every purchase over $20. Record what you were feeling before buying. You’ll start to see patterns: boredom, stress, celebration.

- Replace the Habit — If you shop to relieve stress, find another activity that gives you a dopamine hit without hurting your wallet — a workout, cooking, or even reorganizing a room.

- Add Friction — This might sound silly, but wrapping your card in a sticky note with a reminder like “Do you really need this?” can create just enough pause to rethink.

The Social Media Effect on Card Spending

Instagram, TikTok, and other platforms aren’t just entertainment — they’re marketing machines. Influencers show “hauls” and “unboxings,” brands target you with personalized ads, and you’re constantly seeing curated lifestyles that seem attainable with just a few purchases.

The problem? Those purchases don’t come with the reality behind the scenes — the debt, the returns, the buyer’s remorse. Credit cards make it easy to join the game without thinking about the consequences.

One way to fight this is to curate your feed. Unfollow accounts that push you toward unnecessary spending and replace them with content that inspires healthier habits, whether it’s financial advice, DIY projects, or travel tips that focus on budget-conscious adventures.

Rewards Programs: The Sweet Poison

Points, miles, cashback — they sound like free money. But rewards programs are carefully calculated to encourage you to spend more than you otherwise would.

For example, if you’re chasing a free flight that requires 50,000 points, and you’re just 5,000 points short, you might spend an extra $1,000 to get there — forgetting that you could have just bought the ticket outright for less.

The trick to winning at rewards is to flip the equation:

- Use the card for purchases you were already going to make.

- Pay it off immediately so you don’t incur interest.

- Never buy something just for the points.

If you can stick to that, rewards can truly benefit you — but the moment you start justifying extra spending “for the miles,” the program is winning, not you.

Why Minimum Payments Are a Trap

The minimum payment exists for one reason: to keep you in debt longer.

When you pay only the minimum, you’re covering a small part of the principal and mostly paying interest. Over time, this means a $500 purchase can cost you double or triple if you let it roll over month after month.

The psychology here is clever: the minimum payment makes your debt feel smaller and more manageable, so you’re less motivated to pay it off quickly.

To break this, ignore the “minimum due” line and set your own “full balance” rule — even if it means spending less overall so you can always clear the slate each month.

The Role of Identity in Spending

We don’t just buy things because we need them — we buy them because of who we believe we are, or who we want to be. Credit cards give you access to that version of yourself faster.

If you see yourself as a traveler, you might justify booking more trips on your card. If you identify as a foodie, you might swipe for more dining experiences. These purchases feel like investments in your identity, which makes them even harder to resist.

The way to manage this is to consciously choose identities that align with your financial goals. See yourself as a “savvy investor” or “strategic spender” and you’ll naturally start making purchases that fit that image.

dvanced Strategies to Make Your Card Work for You

Once you understand how your brain responds to credit card spending, you can start turning those same mechanisms to your advantage. Instead of being at the mercy of marketing tactics and emotional triggers, you become the one in control.

Here are some advanced techniques that actually work in real life:

1. Automate Full Payments

The simplest way to avoid falling into the interest trap is to remove the decision entirely. Set up automatic payments for the full balance every month. This makes carrying a balance impossible and forces you to live within your means.

2. Use Separate Cards for Separate Goals

If you travel often, have one rewards card specifically for flights and hotels, and another low-interest card for emergencies. The mental separation makes it easier to track spending and benefits.

3. Pair Credit With Cash-Tracking Apps

Apps like YNAB (“You Need a Budget”) or Mint can sync with your cards and show your spending in real time. This reintroduces the “pain of paying” by giving you constant visibility.

4. Flip Rewards Into Savings

Instead of redeeming points for products or flights right away, cash them out (if your program allows it) and send that money directly into a savings or investment account.

5. Set an ‘Impulse Buffer’

Create a small, separate bank account for unplanned purchases. Transfer a set amount there each month. If you want something on impulse, you have to move the money from that account to pay the card. This adds friction and forces reflection.

Real-Life Example: How Laura Turned Her Spending Around

Laura, a 34-year-old marketing manager, used to carry a $5,000 balance on her credit card. She wasn’t reckless — most of her purchases were “small” things: dinners out, clothing sales, concert tickets. But they piled up.

Once she learned about the pain-of-paying effect, she made two simple changes:

- She started paying with cash for anything under $50.

- She removed her credit card from all online stores.

Within six months, her balance was down to zero. She still uses her card for travel rewards, but now every charge is intentional.

Why Awareness Is Your Greatest Tool

The truth is, credit cards aren’t inherently bad. They can build your credit score, protect your purchases, and even earn you money in rewards — if you know how to manage them.

But the system is built on the assumption that you won’t. That you’ll fall for the dopamine rush, the emotional triggers, the marketing tactics. If you do nothing, the odds aren’t in your favor.

Awareness changes that. When you know the traps, you see them coming. And once you see them, they lose much of their power.

Final Thoughts: Outthinking Your Own Brain

Using a credit card well is less about financial discipline and more about psychological discipline. It’s about recognizing when you’re being nudged toward a decision that benefits someone else more than it benefits you.

So here’s your challenge: for the next 30 days, track every purchase you make with your card. Write down the reason you bought it, how you felt before, and whether you’d still buy it if you had to hand over cash.

By the end of the month, you’ll have a map of your spending mind — and once you can see the map, you can start rewriting the route.

Credit cards will always be powerful tools in the hands of banks and retailers. But with the right awareness, habits, and strategies, they can be even more powerful in your hands.

Deixe um comentário